Personal Interests

- Music — Piano & Viola

- Languages — Spanish (Native), English (C1), Portuguese (B2), French (B1), Mandarin Chinese (HSK3)

- Scuba Diver

Strongest Skill

Turning quantitative ideas into reality.

Quant Finance Certifications

- Advanced Calculus for Finance — Baruch College European Options, Arbitrage-Free Pricing & Arbitrage, Delta/Gamma Hedging, Implied Volatility, Bond Math, Portfolio Optimization

- Numerical Linear Algebra for Financial Engineering — Baruch College Arrow-Debreu Model. Risk-neutral pricing,Complete and incomplete markets - binomial and trinomial trees,Covariance and correlation matrices from time series data,Portfolio optimization theory. Efficient frontier and tangency portfolio,Value-at-Risk (VaR). Portfolios with multivariate normal asset returns. Portfolio VaR.

- Partial and Ordinary Differential Equations with Applications to Financial Engineering — Baruch College Differential equations and the term structure of interest rates, Bond default probability model, Perpetual American options solution, The derivation of the Black-Scholes PDE, Boundary conditions, Financial interpretations, The solution to the Black-Scholes PDE and the derivation of the Black-Scholes formulas, Extensions of the Black-Scholes PDE

- C++ for Financial Engineering — QuantNet (Modern C++ practices for quant finance)

- Probability Theory for Financial Applications — Baruch College Binomial asset pricing model, Risk and expected return of a portfolio, Black-Scholes model, Risk-neutral probabilities, Options pricing, Monter-Carlo simulation

- P Exam (Probability) — Society of Actuaries Discrete distributions, Continuous distributions, Computation of expectations, variances and generating functions, joint distributions, conditional distributions and conditional expectations, Law of large numbers, Central limit theorem

Tech Certifications

Hard Skills

- Machine Learning Engineering (6+ years with data products)

- Data Engineering (6+ years with data products)

- Cloud Computing

- Futures Trading (4 years hands on experience)

- Options Trading (1.5 year hands on experience)

- Python (10/10), SQL (10/10), Data Visualization (10/10), C++ (8/10), Java (7/10), Go (7/10), C# (5/10)

- Stochastic Calculus, Option Pricing, Monte Carlo, PDEs & Finite Differences

- Statistical Inference, Hypothesis Testing, Linear Regression

Live Projects

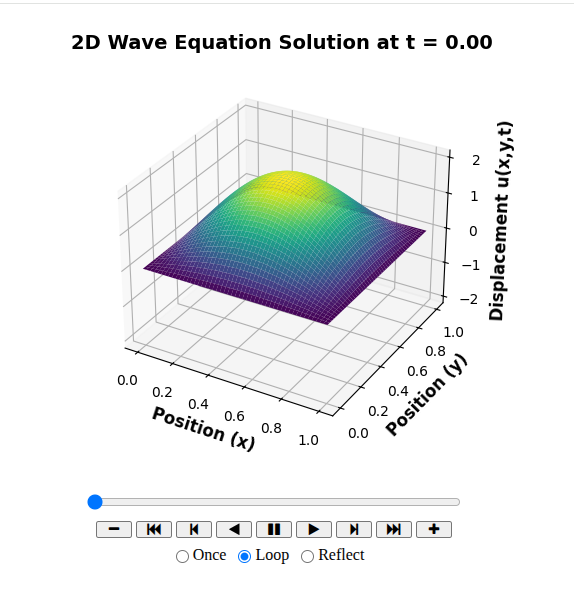

Two Dimensional Wave Simulation Using FDM

This project showcases a numerical simulation of the 2D wave equation using the Finite Difference Method, paired with a smooth, dynamic animation. A vibrating membrane with fixed ends is modeled from first principles and validated against its exact analytical solution, ensuring both accuracy and insight. The result transforms a classic PDE from static math into a living system you can watch evolve in time. It’s a concise, elegant demonstration of how physics, computation, and visualization come together to make waves literally move.

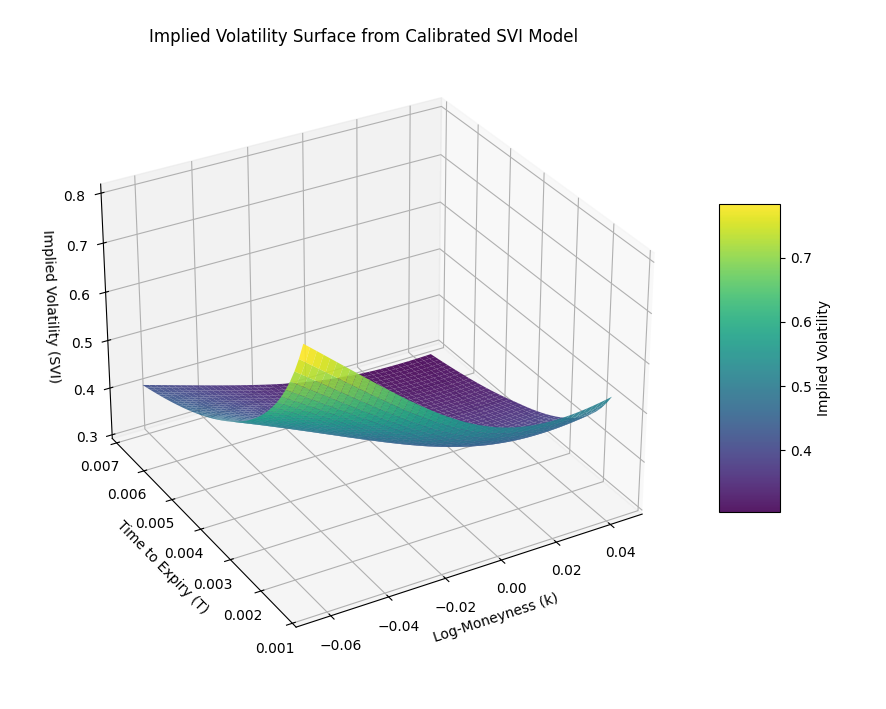

Bitcoin Options Live Snapshot Volatility Surface

Capture a live snapshot of Bitcoin options, build intuition from the Black–Scholes baseline, then fit the smile using the Stochastic Volatility Inspired (SVI) framework.

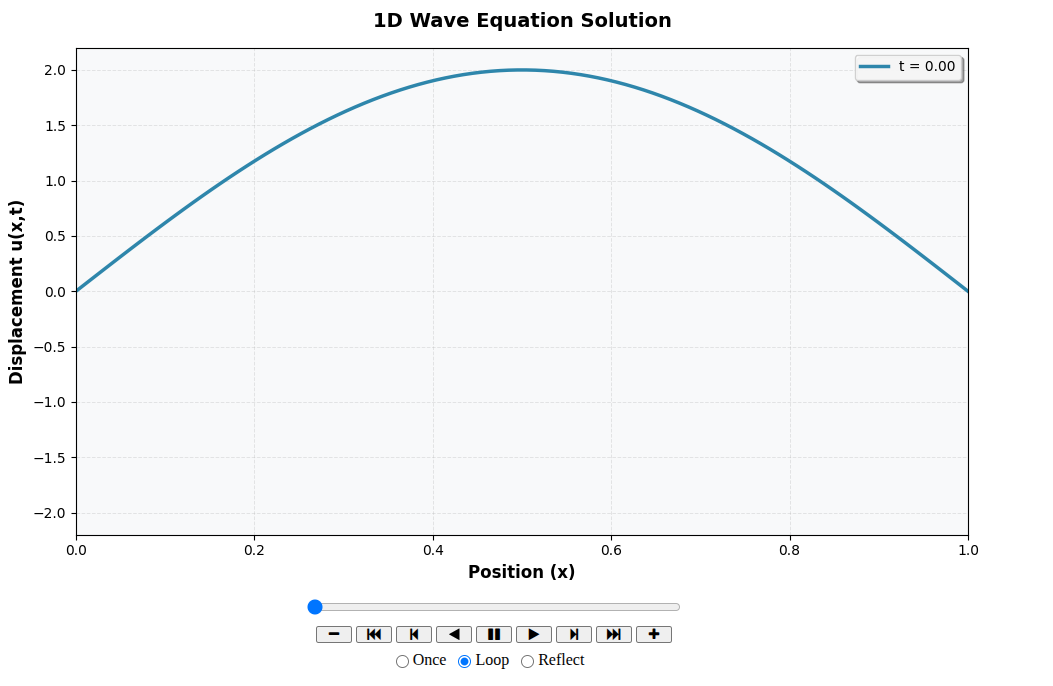

One Dimensional Wave Simulation Using FDM

This project showcases a numerical simulation of the 1D wave equation using the Finite Difference Method, paired with a smooth, dynamic animation. A vibrating string with fixed ends is modeled from first principles and validated against its exact analytical solution, ensuring both accuracy and insight. The result transforms a classic PDE from static math into a living system you can watch evolve in time. It’s a concise, elegant demonstration of how physics, computation, and visualization come together to make waves literally move.